OCULAR THERAPEUTIX (OCUL)·Q4 2025 Earnings Summary

Ocular Therapeutix Misses Revenue But Eyes Pivotal SOL-1 Data Readout in Weeks

February 5, 2026 · by Fintool AI Agent

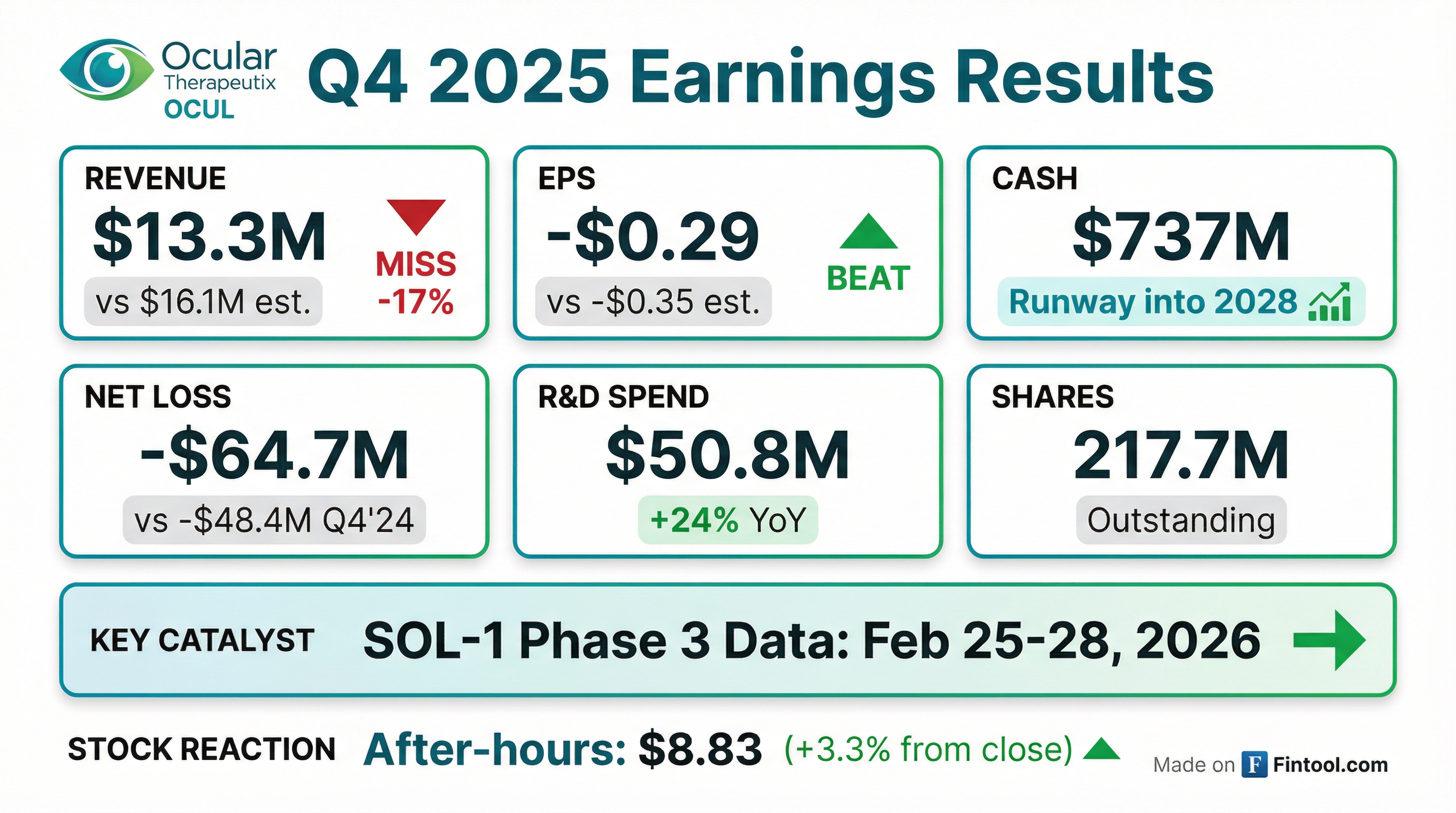

Ocular Therapeutix reported Q4 2025 results that missed revenue expectations by nearly 18%, but delivered a smaller-than-expected loss. The real story isn't the quarter—it's the imminent SOL-1 Phase 3 data readout for AXPAXLI in wet age-related macular degeneration (wet AMD), expected at the Macula Society meeting in just three weeks.

The company declined to host an earnings call, citing a "quiet period" ahead of the catalyst.

Did Ocular Therapeutix Beat Earnings?

Mixed results: Revenue missed substantially while EPS came in better than feared.

Revenue declined 22.4% year-over-year from $17.1M in Q4 2024, driven by a "significantly more challenging reimbursement environment" for DEXTENZA, the company's commercial ophthalmic product. Despite recording its highest annual unit volume in product history, net revenue pressures weighed on results.

Full year 2025: Revenue of $52.0M, down 18.5% from $63.7M in 2024. Net loss widened to $(265.9M) from $(193.5M).

What's Driving the Loss Expansion?

R&D spending surged as OCUL advances its Phase 3 pipeline toward the finish line:

Full-year R&D jumped 54% to $197.1M from $127.6M, reflecting the SOL-1, SOL-R, and HELIOS-3 clinical trials plus pre-commercial AXPAXLI investments.

How Did the Stock React?

The stock rose +3.3% after hours to $8.83, up from the $8.55 close. This is notable given the revenue miss—suggesting the market is squarely focused on the upcoming SOL-1 catalyst rather than current financials.

OCUL has been volatile, trading between $5.79 and $16.44 over the past 52 weeks. The stock is down roughly 47% from its 52-week high.

The Main Event: SOL-1 Phase 3 Data

All eyes are on the SOL-1 Phase 3 superiority trial, with Week 52 results expected at the 49th Macula Society Annual Meeting (February 25-28, 2026).

Why this matters:

- SOL-1 is being conducted under an FDA Special Protocol Assessment (SPA) agreement

- If positive, OCUL plans to submit an NDA for AXPAXLI in wet AMD based on this single trial

- The trial has the potential to support the first label with a superiority claim over aflibercept (2 mg) for any wet AMD product

- All 344 subjects have completed Week 52 visits and been re-dosed

- Patient retention remains "exceptional" with per-protocol rescues

Trial design: The primary endpoint is the proportion of subjects maintaining visual acuity (loss of <15 ETDRS letters) at Week 36. Subjects received either a single dose of AXPAXLI or aflibercept (2 mg) after an 8-week loading phase.

The stakes: Wet AMD affects 14.8 million people globally and 1.7 million in the US. Current anti-VEGF treatments require frequent injections with up to 40% patient discontinuation within one year. AXPAXLI's bioresorbable hydrogel design could offer a differentiated treatment paradigm.

Pipeline Updates

SOL-R acceleration: The non-inferiority trial completed randomization in December 2025 with 631 subjects (exceeding the 555 target), pulling forward expected topline data to Q1 2027.

HELIOS-3: This Phase 3 trial in moderately severe to severe non-proliferative diabetic retinopathy (NPDR) initiated in November 2025. Depending on FDA discussions about AXPAXLI's wet AMD filing plans, OCUL may pursue a streamlined single-trial approach in diabetic retinal disease.

Cash Position and Runway

OCUL ended Q4 with $737.1 million in cash, a significant increase from $392.1M a year earlier following the September 2025 equity offering that raised approximately $475 million gross ($445.6M net).

Management stated this cash balance is "sufficient to support planned expenses, debt service obligations, and capital expenditure requirements into 2028"—covering the SOL-1, SOL-R, HELIOS-3, and potential HELIOS-2 readouts, SOL-X initiation, and pre-commercial AXPAXLI investments.

Caveat: The runway projection does not include full commercialization expenses if AXPAXLI is approved.

What Changed From Last Quarter?

Key developments since Q3:

- SOL-R randomization completed with 631 subjects (December 2025), accelerating timeline

- HELIOS-3 initiated in November 2025

- Company entered quiet period ahead of SOL-1 readout

Key Risks

- Binary catalyst risk: SOL-1 data will make or break the stock in weeks

- Regulatory uncertainty: Even with positive data, FDA may require additional trials or impose label restrictions

- Commercial execution: DEXTENZA reimbursement challenges signal potential headwinds for AXPAXLI commercialization

- Dilution: Share count up 38% YoY following the equity raise

- Competition: Reference pricing regimes could impact AXPAXLI's commercial potential outside the US

Forward Catalysts

Bottom Line

Q4 2025 financials are almost irrelevant. Ocular Therapeutix is a binary bet on AXPAXLI's Phase 3 data, and the verdict arrives in three weeks. The company is well-capitalized with runway into 2028, but the DEXTENZA revenue headwinds highlight the commercial execution challenges that await even if the clinical program succeeds.

The after-hours pop suggests the market agrees: this is all about SOL-1.

Data sourced from Ocular Therapeutix 8-K filed February 5, 2026 and S&P Global.